ABC of NPS

Annuity is a financial product being offered by Annuity Service Providers (ASPs) that provides periodical payments upon your exit from the NPS scheme. The subscriber chooses ASPs to manage annuity funds and payment of pension after you attain the age of 60 years or superannuation. There are different types of annuities.

NPS offers several benefits to its subscribers:

- Market-Linked Returns across asset classes such as equities, corporate bonds and government securities

- Flexible Contributions

- Portability

- Tax Benefits

- Choice of Fund Managers and Investment Options

Contribution refers to the money that a subscriber puts into their NPS account. The contribution may be voluntary or a percentage of the salary. These contributions are invested in a mix of equity, corporate bonds, liquid funds and government funds based on the subscriber’s choice.

In NPS, diversification is achieved through allocation of funds across asset classes – Equity, Gilt and Corporate Bonds based on the subscriber's risk tolerance, investment horizon, and financial goals and can be selected through Auto choice or Active choice

NPS follows the Exempt-Exempt-Exempt (EEE) tax status. Here's what each "E" signifies:

Exempt at Contribution (First E): Contributions made by individuals to their NPS accounts are eligible for deductions under certain sections of the Income Tax Act.

Exempt at Accumulation (Second E): The returns and gains on the investments made within the NPS accumulate tax-free. This means that the growth of the invested amount is not subject to any capital gains tax during the accumulation phase.

Exempt at Withdrawal (Third E): At the time of withdrawal, a certain portion of the accumulated corpus is mandatorily used to purchase an annuity, and the remaining amount can be withdrawn as a lump sum. The lump sum withdrawal is also tax-exempt.

NPS is Flexible. You can invest in NPS via an SIP or ad hoc contributions or corporate deductions. Start with as low as INR 1000 per year in contribution.

G Sec refers to Government Securities. These are debt instruments issued by the Government of India to raise funds. They are considered low-risk investments.

Within NPS, subscribers have the option to invest in different asset classes, and one of the choices is Government Securities (G Sec).

Happy retirement with NPS not only represents the culmination of a successful professional journey but also the assurance of a confident and comfortable future. Prudent financial planning early in your career can ensure a content and worry-free retirement

NPS subscribers have the flexibility to choose their fund manager from among the Pension Fund Managers (PFMs) appointed by the Pension Fund Regulatory and Development Authority (PFRDA).

Subscribers can also select their preferred investment options, such as Active Choice (self-managed) or Auto Choice (age-based automatic asset allocation).

Maintaining one's lifestyle after retirement is crucial for ensuring a comfortable and fulfilling post-working life. By carefully planning and investing for retirement, individuals can avoid a decline in their standard of living and enjoy the fruits of their lifelong efforts.

-Jaisa aaj, Waisa kal

Your KYC in NPS will be done using Aadhaar through One Time Password (OTP) authentication. OTP for the purpose of authentication will be sent to the mobile number registered with the Aadhaar.

Average life spans are increasing in India. Hence, you are likely to spend longer retirement years. Therefore, it is important to plan well and invest early for a comfortable retirement

Market-linked returns refer to the performance of the investment portfolio based on the market movements. The returns on the portfolio are not fixed but depend on the performance of the underlying market.

National Pension System (NPS) is a voluntary, defined contribution savings scheme designed to help subscribers invest for their retirement. The scheme encourages people to invest regularly during their working years.

Opening an NPS account is easy. You can open an NPS accounts through

- POPs (Points of Presence) - can be banks, financial institutions, and other entities registered with PFRDA

- Central Recordkeeping Agency (CRA) - Protean, Kfintech and CAMS.

Your Permanent Retirement Account Number (PRAN) is unique to you for lifetime. If you change jobs or move anywhere, you can continue to invest with the same PRAN. The PRAN is portable across employer.

Based NRI?

Qatar Based NRI? No problem. Any Indian Citizen including NRIs and OCI (Overseas Citizen of India) can open an NPS account.

NPS is regulated by the Pension Fund Regulatory and Development Authority.

As per existing PFRDA guidelines, subscribers on exit can opt for withdrawing maximum 60% of the corpus as lumpsum and minimum 40% to purchase as annuity at exit.

- Recently, PFRDA has introduced the Systematic Lumpsum Withdrawal (SLW) facility which allows subscribers to gradually withdraw up to 60% of their pension savings, giving them flexibility and control over their finances in retirement. The SLW facility will be available only on Superannuation and only on the lumpsum portion.

- With SLW, NPS subscribers can now dip into their pension pot on a monthly, quarterly, half-yearly, or annual basis – until they hit the age of 75.

NPS offers attractive tax benefits.

- Deduction of up to Rs 1.5 lakhs under Section 80 CCD (1) of the Income Tax Act.

- A further deduction of up to Rs. 50,000 under Section 80 CCD (1B) of the Income Tax Act exclusively for NPS investments.

- Further, subscribers under Corporate NPS model can get additional tax benefits under section 80CCD (2) of the Income Tax Act on investment up to 10% of Basic Salary ( old tax regime) or up to 14% of Basic Salary ( new tax regime). This benefit is capped at Rs 7.5 lakhs (including PF, Superannuation fund and NPS).

All the above tax related exemptions are applicable to those who take benefits under the old income tax regime.

Contributions to NPS are eligible for deductions under Section 80CCD (2) of the Income Tax Act under the new tax regime.

PRAN

Once you open an NPS account, you will receive a unique 12 digit Permanent Retirement Account Number (PRAN). Once allotted, the PRAN cannot be changed.

NPS is a voluntary, long-term retirement savings scheme which aims to provide retirement income to subscribers. While participation in the NPS is voluntary, it has gained popularity as a retirement savings option.

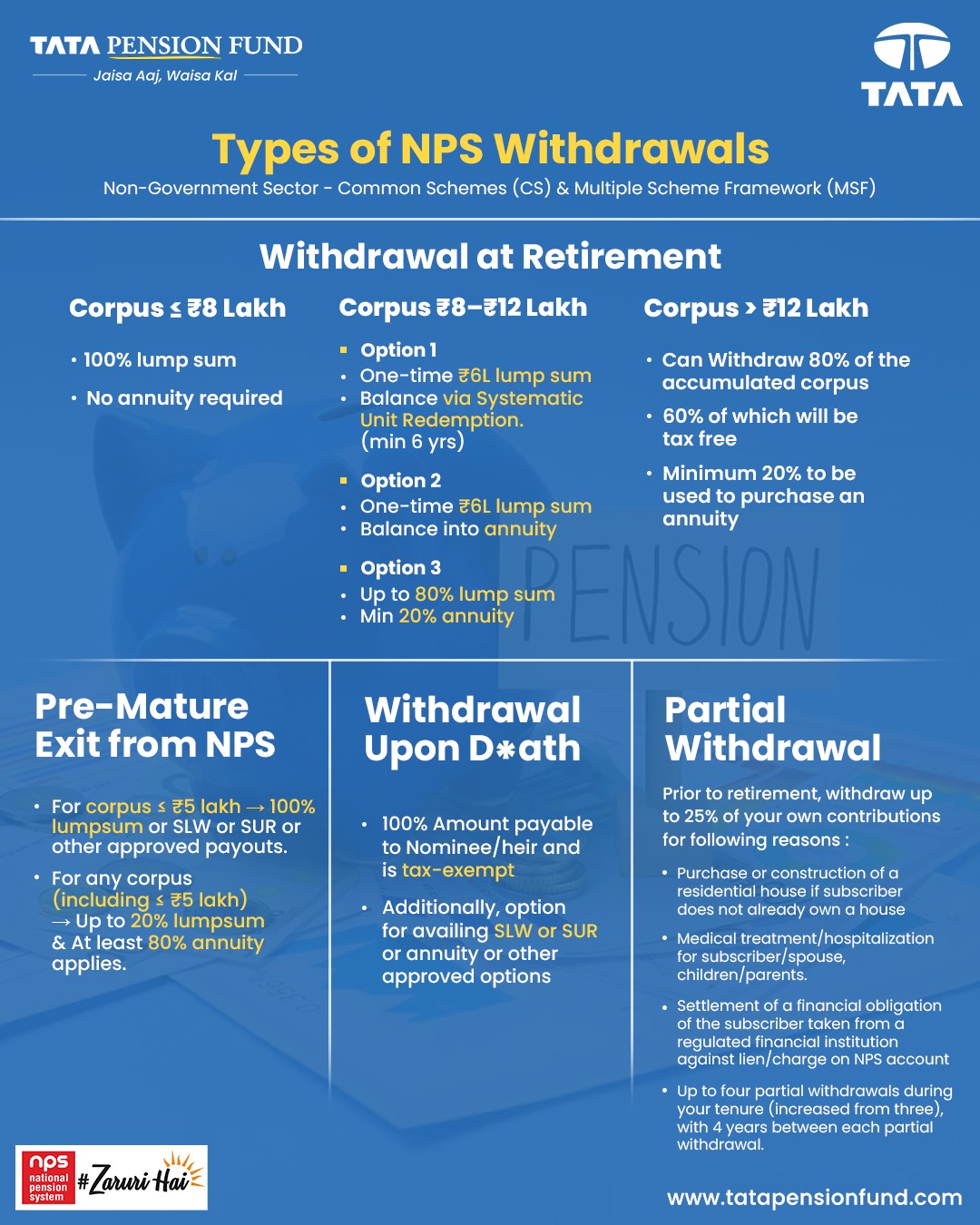

Withdrawing money from your NPS Account

- For Non-Government sector subscribers under Common Scheme (CS) and Multiple Scheme Framework (MSF), exit and withdrawal rules are based on your corpus and exit type.

- If you're over 60, you can choose to hold off on the annuity and lumpsum withdrawal until you hit 85.

Click the button below to see the complete details in the attached document

ratio

NPS is one of the lowest cost pension schemes in the world.

You Only Retire Once. So, invest wisely for your retired years.

You can open an account digitally as NPS registration can be done with zero paperwork. All you need is your Aadhaar Number, Scanned copy of PAN card, scanned copy of cancelled cheque and your scanned signature. That’s it.